Disassembly Cost Calculation

In circular processes like refurbishing and remanufacturing, a used product is normally the initial object. The

first step in the process is to disassemble this product into components. By disassembling, refurbishing and

reusing components, similar products can be built at a significantly lower cost and with less environmental

impact.

It is important to be able to calculate the standard cost for these disassembled components. The calculation is

done by distributing all material and disassembly operation costs for a product to all the components that can be

expected to be reused.

Disassembly Component Standard Cost

The disassembly component is a part that is being produced by disassembling another part, normally a used product e.g. a scrapped engine.

A disassembly component is identified by a specific inventory part type, Disassembly Component.

Standard Cost for a disassembly component can be calculated based on the cost for the part that is being

disassembled and the cost for the operations needed for the disassembly process. Sometimes additional components

are needed to perform the process and then the cost for those must be included. This is a significant difference

from the normal manufacturing cost calculation where the cost is accumulated from all its components and

operations. In the disassembly case the cost is instead distributed to multiple components that result from the

disassembly process.

Disassembly Standard Cost calculation requires the following data to be correctly set up.

Disassembly Structure

A product structure of type Disassembly must exist, valid for the effective date with a * alternate in status Plannable or Buildable. Components that come out from the process are registered on the Produced Parts tab in Product Structure page. Additional components needed for the process are registered in the Components tab.

For each disassembly component, the following parameters can be registered to control the cost calculation.

Operation Cost Distribution Factor

This factor controls how much of the total operation costs will be distributed to a certain component.

General Overhead Distribution Factor

If general overhead is used this factor controls how much of the general overhead costs will be distributed to a certain component.

Scrap Factor

The scrap factor defines, for each disassembled component, to which extent that part is expected to not be possible to reuse. Expected scrap will increase the cost for a component according to a factor 1/(1 - Scrap Factor).

Cost Distribution

In Component Cost Distribution tab the Cost Distribution factor is defined for each disassembled component. The cost for input components can be distributed individually so the cost for the disassembled part is distributed in one way and other additional components are distributed in another way.

Disassembly Routing

A product routing of type Disassembly must exist, valid for the effective date with a * alternate in status Plannable or Buildable.

For each operation, the following parameters can be registered to control the cost calculation.

Operation Quantity Factor

The operation costs are calculated in the same way as for a manufactured part with the addition of the operation quantity factor set for each operation line. This parameter is used by the disassembly process. The Operation Qty Factor field indicates proportion of the total order quantity that normally pass this specific operation, e.g. a cleaning operation that is sometimes needed and sometimes not.

Other cost impacting data

Other part related data will impact cost calculation in the same way as in traditional cost calculation, i.e. it will build up cost for the parent part which is then distributed to the disassembly components. This data includes: Standard lot size and Scrap Factor (%) for Inventory Part, Scrap Factor (%) and Component Scrap for Product Structure. It also includes Delivery Overhead, Material Overhead and General Overhead.

For further information about part cost calculation see more in About Part Cost Calculation.

Cost Templates

Disassembly Components

The disassembly cost calculation is based on the parts that are being disassembled. This means that cost is calculated for the top part and pushed to the components rather than calculated at component level and fetched from the parent. This also means that the content of cost buckets in the cost template for the disassembled components is of lesser importance since the components will inherit the buckets from the parent.

An exception from this is when disassembly is performed in two steps. The cost template then also needs to pick up operation costs for the second level disassembly.

It is important that the disassembled components have a cost template with the toggle switch Use Cost Distribution enabled. Otherwise, it will be calculated using normal part cost calculation. This setup can be used for a manually added cost for the disassembly component which would then be entered as an estimated part cost for the component.

A standard cost template D-110 is created when registering a new site. It is the default cost template for new inventory parts with part type Disassembled Component. This template has Use Cost Distribution set and contains the standard manufacturing cost buckets. If the estimated cost should be used, the cost template must contain a bucket for the estimated cost, e.g. standard Cost Template P-110 can be used.

Disassembled Part

For the part that is being disassembled the cost template serves two purposes

- Control the cost calculation for the part itself.

- Control the cost calculation for disassembling the part.

Typically, the disassembly parts will be purchased and therefore need an externally acquired cost bucket, e.g.

110. It is also important that the Cost Rollup Control flags Use External Acquired Costs

is enabled and Use Manufacturing Costs is disabled.

In order to pick up the operation costs for disassembly, the manufacturing cost buckets need to be included. These

will be used by the disassembly cost calculation if Use Manufacturing Costs is

disabled.

An easy way to create this cost template is to copy the M-110 template, add a procurement bucket (110, 120, 130 or 140) and switch the cost rollup from Use Manufacturing Costs to Use External Acquired Costs.

Produced Part Cost Base

A certain disassembled component could sometimes originate from various parents. However, the calculated cost will always originate from only one parent. In case there are more than one you need to select which one to use for the calculation. This is done on the Produced Part Cost Base tab, on Part Cost page. This tab lists all possible parents based on existing plannable or buildable Produced Part structures. Note! This tab also point to which material line to use for calculation, which means that in case the same part exists on multiple lines in a structure, the cost will only be based on the selected line.

Calculation

The disassembly cost calculation is performed by Disassembly Cost Calculation. Before the calculation of disassembly cost it is important that the cost for the disassembled products and input components are correctly calculated. This means that a traditional cost calculation should be performed prior to the disassembly cost calculation.

The disassembly cost calculation will look for any part, according to the selection criteria, that has a valid (buildable or plannable) disassembly structure on the effective date. For each structure found, the calculation will be performed in a top-down manner. This means the cost for the parent and other components plus operation costs according to the routing and defined overheads according to the parent’s cost template will be distributed to the disassembled components according to the distribution factors. Only components that have a cost template with Use Distribution Cost set will be updated.

If any of the disassembly components, which have their cost updated according to the above, has its own valid disassembly structure the calculation will continue with the newly updated cost as input.

Examples

Example 1

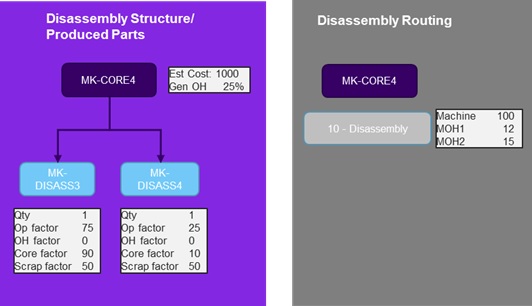

In this example the parent MK-CORE4 is disassembled and each MK-CORE4 gives one MK-DISASS3 and one MK-DISASS4. However, in 50% of the cases those will not be possible to reuse so the scrap factors are set to 50%

The disassembly process is performed in one operation with a machine time of just 1h and the work center cost 100/h with OH1 of 12 per unit and 15 per batch.

Costs are distributed differently for material and operations according to the factors below.

Picture 1 - Disassembly example 1, set up

The resulting cost for the disassembled components will then be:

(Material cost*Mtrl factor)+(operation cost*Op factor)/(1-Scrap factor)

Tot cost MK-DISASS3 = (1000*0.90+(100+12+15)*0.75) / (1-0.5) = 1990.5

Tot cost MK-DISASS4 = (1000*0.10+(100+12+15)*0.25) / (1-0.5) = 263.5

Assuming a template with standard manufacturing cost buckets (E.g. copied from M-110) is used for MK-CORE4 this cost is distributed to cost buckets according to the table below.

| Bucket | MK-DISSASS3 | MK-DISASS4 |

| 110 - Estimated Material Cost | 1800 | 200 |

| 300 - Machine Cost | 150 | 50 |

| 321 - Machine Overhead1 Cost | 18 | 6 |

| 322 - Machine Overhead2 Cost | 22.50 | 7.50 |

Table 1 - Disassembly example 1, resulting costs

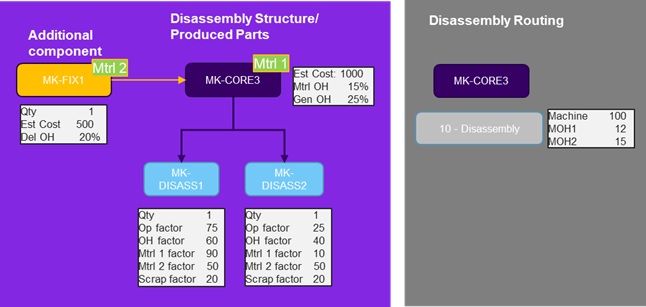

Example 2

This example is similar to the previous, but it has an additional component, MK-FIX1, needed for the disassembly process. Also, delivery, material and general overheads are added.

Picture 2 - Disassembly example 2, set up

Resulting costs for each disassembled component will be calculated according to:

Estimated cost = ((Mtrl1 Est Cost * Mtrl1 factor) + (Mtrl2 Est Cost * Mtrl2 factor)) / (1 - Scrap factor)

Delivery OH = (Mtrl2 Est Cost * Mtrl2 Del OH * Mtrl2 factor) / (1 - Scrap factor)

Machine cost = (Machine Cost * Op factor) / (1 - Scrap factor)

Machine OH1 = (MOH1 * Op factor) / (1 - Scrap factor)

Machine OH2 = (MOH2 * Op factor) / (1 - Scrap factor)

Mtrl OH = (Mtrl1 Est Cost * Mtrl OH * Mtrl1 factor) (1 - Scrap factor)

Gen OH = ((Mtrl1 Est Cost + Mtrl2 Est Cost + Mtrl2 Est Cost * Mtrl2 Del OH + Machine Cost+

MOH1+ MOH2+ Mtrl1 Est Cost * Mtrl OH) * Mtrl1 Gen OH) * OH factor / (1 - Scrap factor)

Assuming a template with standard manufacturing cost buckets (E.g. copied from M-110) is used for MK-CORE4 this cost will be distributed to cost buckets according to Table 2.

| Bucket | MK-DISSASS1 | MK-DISSASS2 |

| 110 - Estimated Material Cost | 1437.50 | 437.50 |

| DOH20 – Delivery OH 20% | 62.50 | 62.50 |

| MOH15 – Material OH 15% | 168.75 | 18.75 |

| 300 - Machine Cost | 93.75 | 31.25 |

| 321 - Machine Overhead1 Cost | 11.25 | 3.75 |

| 322 - Machine Overhead2 Cost | 14.06 | 4.69 |

| GOH25 – General OH 25% | 351.94 | 234.63 |

| Total Cost | 2139.75 | 793.06 |

Table 2 - Disassembly example 2, resulting costs

Cost Calculation for Alternate Disassembly Components

You can use alternate disassembly components when other than the defined disassembly component in the product

structure are expected to be found during the shop order process. The standard cost of such an alternate

disassembly component can be estimated based on a similar disassembly component defined in a disassembly product

structure.

During the Disassembly Cost Calculation process, the part cost of the main disassembly

component, which is assigned as the cost base, is copied into the alternate disassembly component.

To set up the alternate disassembly component part cost correctly:

- Define the main disassembly component as the Base for Cost Calculation on the Part Cost page, Alternate Disassembly Component Cost Base tab of the alternate disassembly component.

- Ensure that the cost set of the alternate disassembly component has a cost template with Cost Rollup control flag Use Cost Distribution flag enabled (set to True).

- The main component which is assigned as the cost base must receive its part cost from the Disassembly Cost Calculation process.